Modified Duration in Semi-Annual periods converted to Annual

Why is it that to convert a Semi-Annual Modified Duration to an Annual one, we divide by 2 instead of multiplying by 2? Surely it doesn’t imply that the bond price will move more in half a year than in one full year when interest rates shift?

Zero-Coupon Bond Formula + Calculator

Duration and convexity are important bond concepts - Financial Pipeline

:max_bytes(150000):strip_icc()/final111-8868f6c3ce884d28b2a2aea534a65f44.jpg)

Effective Duration: Definition, Formula, Example

Duration and Convexity, with Illustrations and Formulas

cdn./academy/wp-content/uploads/2019/12/

Modified Duration vs: Macaulay Duration: Key Differences - FasterCapital

How to convert monthly interest rates to annual or yearly rates and back

:max_bytes(150000):strip_icc()/modifiedduration.asp_final-7de3023da1ca4823b80828df9e90d486.png)

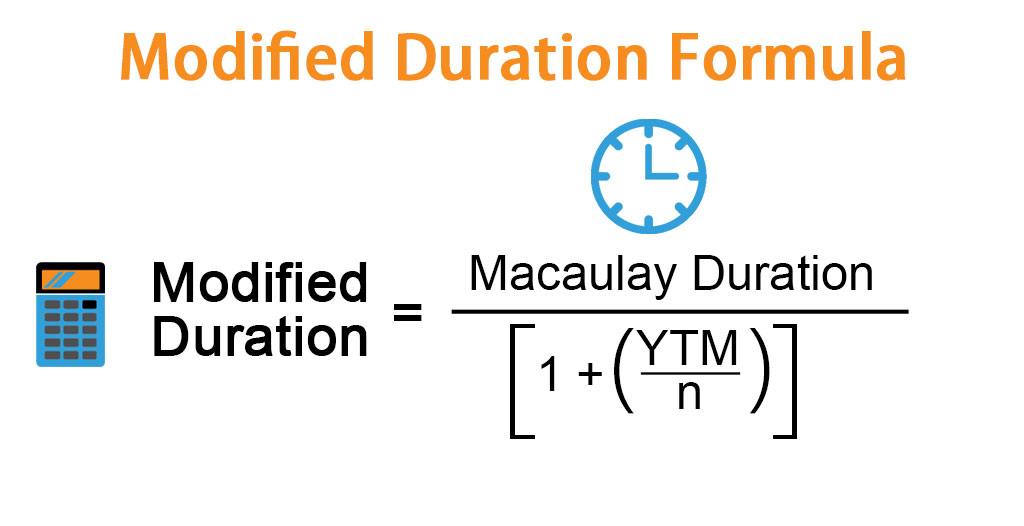

Modified Duration Formula, Calculation, and How to Use It

Duration and convexity are important bond concepts - Financial Pipeline

Convexity of a Bond, Formula, Duration

Yield to Maturity (YTM)

Modified Duration of semi annual coupon bond

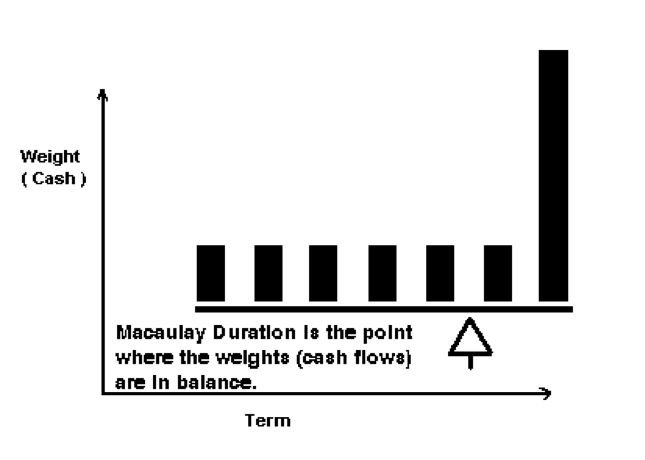

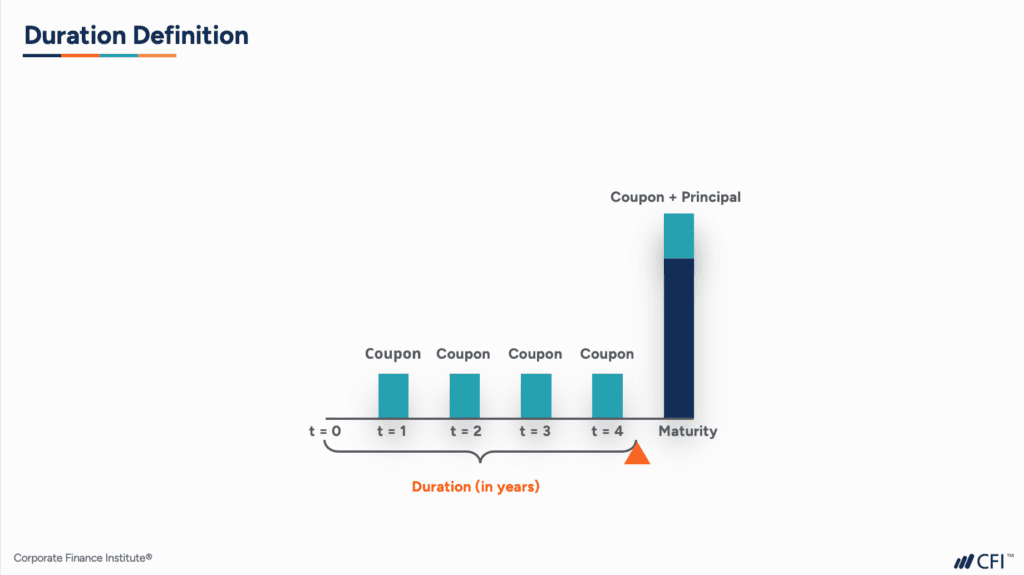

Duration - Definition, Finance, Types, Formulas

How to Calculate Effective Interest Rate: Formula & Examples

Duration - Definition, Finance, Types, Formulas